Closing Recap

Friday, June 02, 2023

|

Index |

Up/Down |

% |

Last |

|

DJ Industrials |

700.99 |

2.12% |

33,762 |

|

S&P 500 |

61.17 |

1.45% |

4,282 |

|

Nasdaq |

139.78 |

1.07% |

13,240 |

|

Russell 2000 |

62.97 |

3.56% |

1,830 |

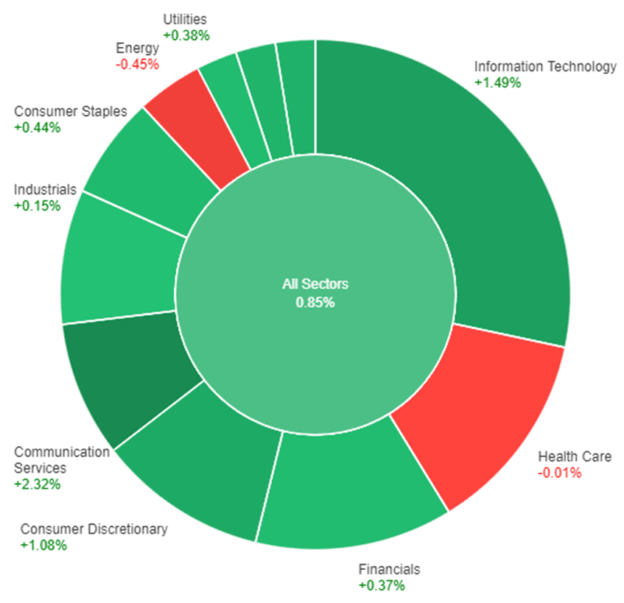

Today good news is good news, but the real question is why? It could be the passage of the debt ceiling bill, or it could be the possibility of a new property support package in China, or it could be the strong nonfarm payrolls report out this morning. The last one is a bit interesting because on any given day, a stronger payroll number could mean more Fed rate hikes and we should see equities in reverse. Today, though, investors appear to prefer the position that more jobs mean more hope for a soft landing. Perhaps after the recent, lackluster commentary about Spring selling season trends from retailers, today’s payrolls data is mostly just a reassurance that the consumer could still have life because more are employed. XRT +4.3% and XLY +245% are decent indicators of consumer spending optimism. That said, leaders were Materials +3.5% and Energy +3.2%, but all S&P sector groups were in the green. Breadth was better than 3:1, favoring advancers despite yields generally moving higher. Heading into the final hour of trading, US equities continued to grind higher. Not much had changed materially in terms of sector leadership. As one would expect, both Growth and Value gained, but Value was the star today with the Russell 1000 Value +2.1% versus the Russell 1000 Growth at +1.4%.

In data points of interest today, @charliebillelo gives a bit of earnings recap, pointing out that with 98% of companies reported, S&P 500 GAAP EPS climbed 6% yr/yr and sales per share rose 9% yr/yr, with both beating expectations. Separately, @KobeissiLetter demonstrates the mega-cap names that seem to rule the market right now also rule how we live, noting Amazon may be moving into mobile phone service for Prime members, Apple will be offering high-yield saving accounts, JP Morgan now controls over 15% of US bank deposits, Google controls over 90% of global search traffic and Meta now has 3 billion active users across their various platforms. The strong have gotten stronger, as have their stocks. Finally, @LizAnnSonders notes only twice in history have payrolls gained at least 300k while the unemployment rate ticked up by at least 0.3% mo/mo. The first was July 1984 and the second was May 2023. Not sure what to do with that, but I bet there are a few folks at the Fed wondering the same thing.

The Nasdaq Composite posts its 6th consecutive week of gains, the longest weekly winning streak since January 2020 as “AI” euphoria has boosted the space, specifically chip related stocks (NVDA, AMD, MRVL, AVGO, etc.) Note in May, the Nasdaq outperformed the Dow by 9.29 percentage points which ranks as the 9th widest margin of outperformance for the Nasdaq relative to the Dow in history” according to Bespoke Investment. Meanwhile the Russell 2000 up 4.46% to start the month.

Economic Data

· Nonfarm payrolls for May surge +339,000 well above consensus +190,000 and vs April +294,000 (prev +253,000), March revised to +217,000 (from +165,000).

· May private sector jobs added +283,000 vs. consensus +165,000

· Unemployment rate rises to 3.7% vs 3.4% previous and estimate of 3.5%

· Average hourly earnings all private workers +0.3% from prior month (in-line with ests.), and US average earnings yoy actual +4.3% (forecast 4.4%, previous 4.4%).

Commodities, Currencies & Treasuries

· WTI crude oil futures were strong throughout the day. The July contract settled off the highs, but still gained $1.64, or +2.34%, to $71.74/bbl. Brent also gained to settle at $76.13/bbl, +$1.85 or +2.49%. Despite today’s gains, WTI futures still posted a loss of 1.3% for the week. Angst around the debt ceiling and corporate earnings had continued to pressure oil ahead of today’s move, so resolution on the debt ceiling combined with better payrolls created a nice relief rally. Traders are now focused on the OPEC+ meeting in Vienna this weekend for visibility into oil’s next move. Consensus into today seemed to be for production policy to remain unchanged, but commentary has been swirling that an additional output cut of about 1Mm barrels per day is also possible.

· While US equities may not have appeared to care much about today’s payroll gains, gold traders looked to be a different story. August gold futures slid by $25.90/oz, or -1.29%, to $1,969.60, generally on concerns the Fed may not be done with rate hikes to manage inflation. Despite today’s slip, the active futures managed a 1.3% gain on the week to end a three-week losing streak. With the debt deal presumably behind us, the June CPI reading is the next big focus for gold, equities, the Fed, etc. At that point, we may get a better read on the Fed pause prospects and expectations through the remainder of the year.

· The US dollar ended the week higher and Treasury yields climbed all day with the 10-year at 3.69% and the 2-yr up over 15-bps to 4.50%. No slowing down stock markets today even with the dollar and yields moving higher following the better jobs data.

|

Macro |

Up/Down |

Last |

|

WTI Crude |

1.64 |

71.14 |

|

Brent |

1.85 |

76.13 |

|

Gold |

-25.90 |

1,969.60 |

|

EUR/USD |

-0.0053 |

1.0708 |

|

JPY/USD |

1.16 |

139.95 |

|

10-Year Note |

0.083 |

3.691% |

Sector News Breakdown

Consumer

Retailers:

· LULU snaps its 9-day losing streak in strong fashion as posted Q1 results ahead of expectations and raised FY23 guidance as 1Q revenue and EPS came in ahead of expectations, with top-line strength across all channels and geographies. China +79% y/y, fuels International +60% y/y, with North America +17% y/y.

· COST reported weaker total comparable sales on a sequential basis, as total comparable sales fell (-0.3%) in May, compared to an increase of +1.4% in April.

· FIVE reported healthy 1Q results but mixed relative to Street expectations, with EPS above but sales below, comps increased 2.7%, while 2Q guidance was issued below consensus and 2023 guidance was narrowed.

· TLYS Q1 EPS loss (-$0.40) vs. est. loss (-$0.33); Q1 revs $123.6M vs. est. $123.75M; guides Q2 EPS loss (13c-27c) vs. est. 0c; revs $148M-$158M vs. est. $160.5M.

Autos, Leisure, Gaming & Lodging:

· In autos: CVNA cancels exchange offer for up to $1 billion of notes; CHPT slipped overnight on lower guide but rebounded; Ford (F) May US EV sales (-13%) as per CNBC; total vehicle May sales rise 10.7% to 170,933 vs. 154.461 units y/y; US truck sales +31.6%; TSLA rising a 6th straight day and highest levels since mid-February.

Energy, Industrials and Materials

· Broad strength in U.S. energy, material, and industrial stocks after a report overnight that China is mulling property market support. Bloomberg reported China is working on new measures to support the property market after existing policies failed to sustain a rebound in the sector. Shares of steel stocks, copper, machinery, iron ore all led markets early.

· In oil services, Baker Hughes (BKR) said the weekly U.S. rig count was down 15 from last week to 696 with oil rigs down 15 to 555, gas rigs unchanged at 137 and miscellaneous rigs unchanged at 4. The U.S. Rig Count is down 31 rigs from last year’s count of 727 with oil rigs down 19, gas rigs down 14 and miscellaneous up 2.

· In trucking and logistics: truckload demand stays weak in sign of freight recession as Bank of America’s said its proprietary bi-weekly Truckload Demand Indicator for shippers’ freight demand outlook for three months out decreased 4% sequentially to 42.6 from 44.3 last survey. The reading was down 27% year-over-year and is the 5th lowest level on record for the survey.

· In chemicals: CC, DD and CTVA announced an agreement in principle to settle all drinking water claims related to perfluoroalkyl and polyfluoroalkyl substances, known as PFAS. As part of the agreement, the companies will establish a settlement fund and contribute a total of $1.185B to the fund, with Chemours contributing about $592M, DD $400M and CTVA about $193M. VVV was downgraded to neutral from Overweight at JP Morgan saying longer-term share multiple risk in Valvoline is likely to stem from long-term growth expectations for electric vehicles.

· In metals: Copper prices post first weekly gain in seven weeks, on track for +2.5% advance after better Chinese factory data a night ago boosted demand hopes while a deal to avert a U.S. debt default boosted stock markets and weakened the dollar (FCX, SCCO, TECK copper names). Uranium names (CCJ, UUUU, UEC) have been moving higher, Reuters noted the U.S. Senate Environment and Public Works Committee advanced a bill on Thursday that would fast-track deployment of advanced nuclear reactors.

· In refiners: Wells Fargo lowered ests/tgts while PBF remain Top Picks; Q2’23 EPS ests exceed consensus across coverage saying following soft start to the qtr, cracks rebounded w the seasonal gasoline uplift; lowers tgts for MPC to $113 (from $124); PBF to $45 (from $48); PSX to $111 (from $118); and VLO to $120 (from $126)

· In industrials, big gains in machinery (CAT) and the like on broader macro bounce in industrials and materials; MMM shares popped late morning on reports said to be in at least $10B PFAS water pollution settlement/settlement awaits board approval, would avoid June 5 trial.

Healthcare

Biotech & Pharma:

· AUTL reports positive top-line data from mid-stage study of obe-cel, therapy candidate to treat a type of blood cancer; said 76% patients achieved complete response meeting primary goal.

· BNTX said its cancer immunotherapy candidate gotistobart, in partnership with OncoC4 Inc, was shown to shrink tumors in close to 30% of participants in an early-to-mid-stage study; said that gotistobart was well-tolerated with manageable safety profile.

· DNA downgraded from Neutral to Sell at Goldman Sachs and cut tgt to $1.25 from $3 as it believes the macro environment and the softening spend it is seeing in the biopharma end market may result in slower new program growth for DNA.

· FGEN upgraded to Buy from Hold at Stifel and raise tgt to $28 from $23 as company is approaching critical data readouts for founding product, pamrevlumab.

Technology

Internet, Media & Telecom

· In Streaming: Keybanc said April streaming monthly churn moved lower to 2.7% compared to a year ago, and modestly decreased 0.1% m/m. When excluding NFLX from KEYB’s data, churn for the traditional Media streaming services also decreased 0.1% m/m at 3.2%. Disney, Hulu, and Peacock improved m/m, while ESPN+, Showtime, and Starz churn increased m/m.

· In Media: WMG was downgraded to Neutral at Atlantic Securities citing the loss of streaming share means recorded music streaming revenues are growing slower than expected, and the rapid development of AI-created music is placing a major cloud over the whole sector.

· In Digital Advertising: TTD upgraded to Overweight saying the co is driving and benefiting from growth in CTV and retail media advertising. With ad markets stabilizing, they see it as well positioned to gain share and drive upward revisions from here.

· In telecom: Bloomberg reported that AMZN is in talks to offer mobile service as well as DISH, to possibly offer low-cost or even free nationwide mobile phone service to Prime subscribers (T, VZ, TMUS shares slide in reaction). The story looks like a follow up from WSJ 5/26 seen here https://tinyurl.com/bdfbbmba

Hardware & Software movers:

· ASAN reported better than expected Q1 results as recent cost cuts drove +10.3pts of QoQ OM improvement; mgmt raised FY24 operating income guidance while reiterating expectations for positive FCF before the end of CY24.

· IOT reported a strong 1Q with 43% rev growth, topping ests by +6.5%

· MDB shares surged as delivered a strong 1QFY24, beating consensus estimates behind robust Atlas (+40% YoY; 65% of revenue), and large customer growth (>100K ARR customers +28% YoY); beat and raise driven by consumption levels that exceeded their outlook.

· PD shares tumble as managed to outperform top-line guidance in the quarter, but by a thin margin, posting $103.2M vs a $103M guidance midpoint; saw increased churn specific to the SMB segment (most of customer base but only 20% of total ARR); guides year revs lower.

· SentinelOne (S) shares fall over 30% after reported mixed F1Q24 results with lackluster revenue of $133.4M (consensus $136.6M), up 70% y/y, and ARR of $563.6M, below expectations of $594.4M; new guidance calls for FY24 revs of $590-600mn vs. prior guide of $631-640mn.

· ZS presented better-than-expected Q3 results relative to the prelim, coming toward or even exceeding, in some cases, the upper end of the guidance for revenue, operating income, and billings; billings of $482.3M (+38% y/y) were above the $478-$482M preliminary guided range.

Semiconductors:

· AVGO reported in-line results Q2 sales/EPS $8.7B/$10.32 met Street while F3Q (Jul) sales outlook inched 2% higher as growth led by networking, up 20% Y/Y; provided additional details on the generative AI opportunity where it expects the opportunity to grow from 10% in FY22 to ~25% in FY24 of semi revenues.

· US listed Chinese technology companies (BABA, BIDU, JD, PDD, TCEHY) advance after headlines overnight that China was weighing up a property market support package to boost the economy.

Market commentary provided by Hammerstone Markets, Inc, a firm separate from and not affiliated with Regal Securities. Regal Securities has not participated in the creation of the content, and does not explicitly or implicitly endorse the content.

The post Market Review: June 02, 2023 first appeared on eOption.