- Netflix to report Q4 earnings on Wednesday 23 after market closes

- Shares finish the year strong; future looks promising too

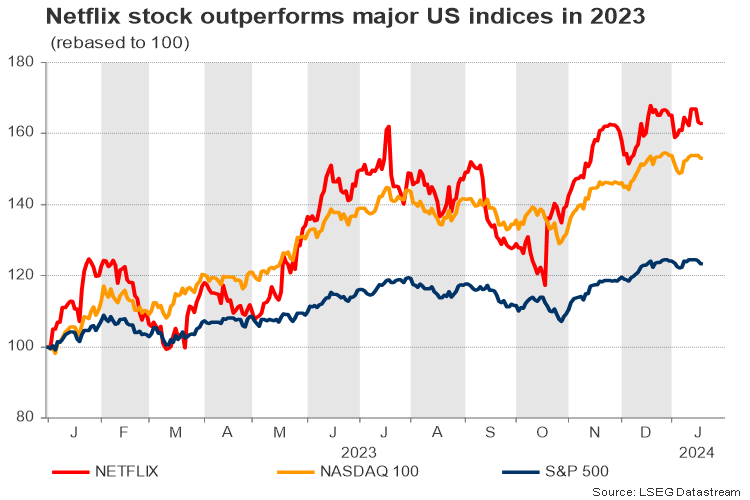

Netflix outperforms major US indices

Netflix’s stock has been in the green almost every single month since the shocking six-month freefall sank the price to a five-year low of 161.38 in June 2022. The pair has recovered more than half of this damage to climb to a high of 502.35 last week, marking a 44.5% gain year-on-year, which is double the S&P 500’s growth of 19.18% and higher than Nasdaq 100’s equivalent of 34.89%.

Forecasts point to strong annual performance

Traders are now eagerly waiting to see whether the streaming giant will further brighten the stock’s outlook when it discloses its Q4 earnings due on Wednesday 23 after the market close. Although the ban on password sharing and the increase in subscription prices angered users, the company’s paid sharing strategy proved a success, boosting net pair membership subscriptions by 5.9 million in the second quarter and 9.0 million in the third quarter, with European, Middle East and African regions contributing the most. Still, average revenue per membership has been growing positively in the US and at a faster pace, even when accounting for currency fluctuations.

Total revenue rose by $8.5 billion in Q3 2023, up from $8.1 billion in Q2 2023 and 7.3 billion in Q3 2022. Net income jumped to $1.67 billion, rising by 12% q/q and 20% y/y, while earnings per share (EPS) increased to $3.80 in Q3, gaining 13% q/q and 21% y/y.

Shareholders were also pleased to hear the company’s encouraging forecasts for the fourth quarter. Despite projections for a relatively flat change in membership additions and average revenue per membership in Q4, total revenue is forecast to rise by 11% to $8.7 billion. This is equivalent to investors’ current expectations and could lift the annual revenue for 2023 to $33.6 billion versus the $31.6 billion reported in 2022. Net income could ease to $985 million in Q4, but still contribute to a 21% yearly increase to $5.4 billion. Earnings per share are expected to fall to $2.22, though lift the annual amount to a new high of $12.18.

Is Netflix stock attractive?

As regards its advertising business, which has been running for almost a year, Netflix is optimistic that the increasing streaming viewing could make it a multi-billion-dollar segment in the long run. Its ads plan membership went significantly up by 70% in the third quarter and more gains in the fourth quarter could be a sign of increasing confidence in the company.

Developing into a multi-language film industry and diversifying its content to advertising, gaming and a future retail sector, Netflix is growing its roots deeper in the ground. Of course, there will be more setbacks on the legal front and more protests from artists as artificial intelligence makes its way into the entertainment world too. Nevertheless, it’s currently difficult to assume that the company will lose the crown in the coming years.

On the financial front, its massive list of subscribers and its first-move advantage may allow Netflix to gain from economies of scale, and also to charge higher prices for a better quality of services in the future. The company is also expecting a higher operating margin of 22-23% in 2024, while its optimism for a growing amount of cash flows might allow more stock buybacks.

As regards valuation, the giant streamer has a P/E ratio of 47.70, which is higher than Apple’s 29.64 and HBO’s 23.30, but significantly lower than Walt Disney’s 71.30 and Amazon’s 78.79. Therefore, valuation is not that expensive compared to its competitors, though it’s possible that persisting recession risks and a fragile geopolitical environment could reduce rewards for shareholders. A maturing business could be a risk to worry in the long-term.

Hence, it’s reasonable that several analysts have upgraded their outlook recently and raised their target price for the stock, with the average recommendation from Refinitiv analysts being a buy at the moment.

Levels to watch

For those who love chart analysis, the short-term picture is sending some discouraging signals for the coming sessions. The price pulled below the 61.8% Fibonacci retracement of the 2021-2022 downtrend after failing twice to stretch successfully above it. A drop below July’s and November’s barrier of $478 and an extension beneath the tentative support trendline at $472.00 could immediately stall near the 50-day exponential moving average (EMA) at $465, though only an extension below the previous low of $445 would officially declare a bearish trend reversal.

Alternatively, a close above the $500 psychological level could initially stall around the $525 barrier and then near the 2020-2021 constraining zone of $550.